正在加载视频...

视频加载失败

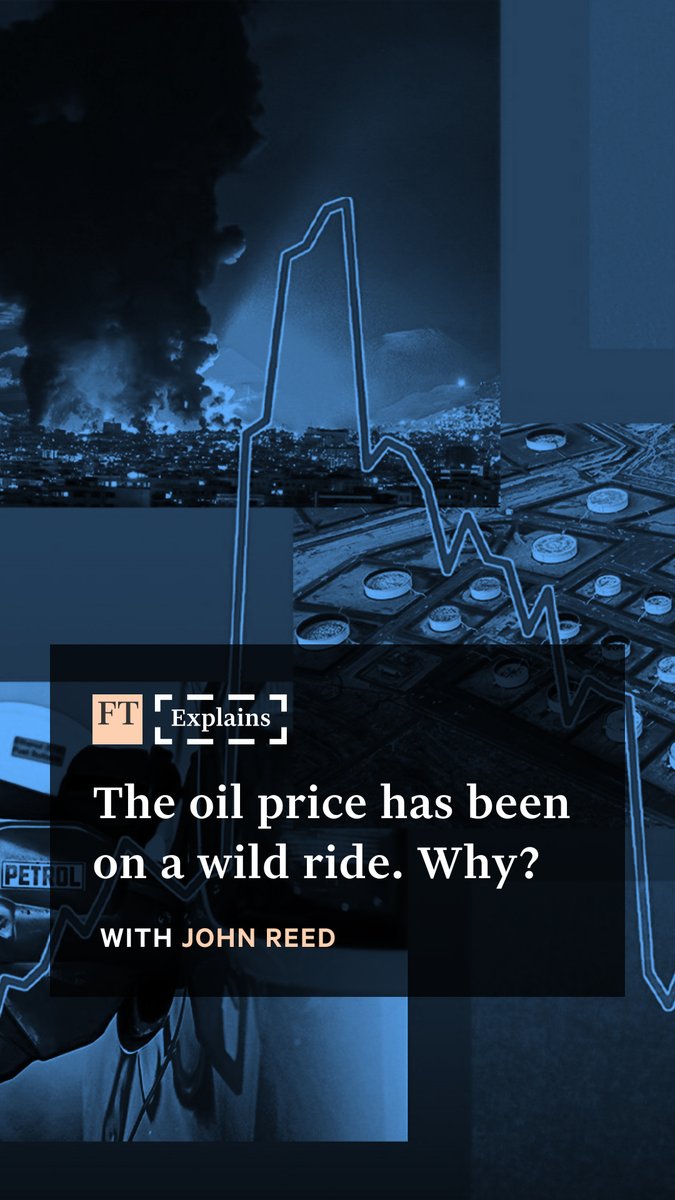

↕️Deconstructing the implied volatility of options and capturing the gap in market expectations 🔺Based on the option smile curve and Monte Carlo simulation, quantitatively analyze the long-short divergence in the options market, and help investors grasp the volatility dividend

0 条评论

暂无评论

原始帖子的评论将显示在这里