Video wird geladen...

Video konnte nicht geladen werden

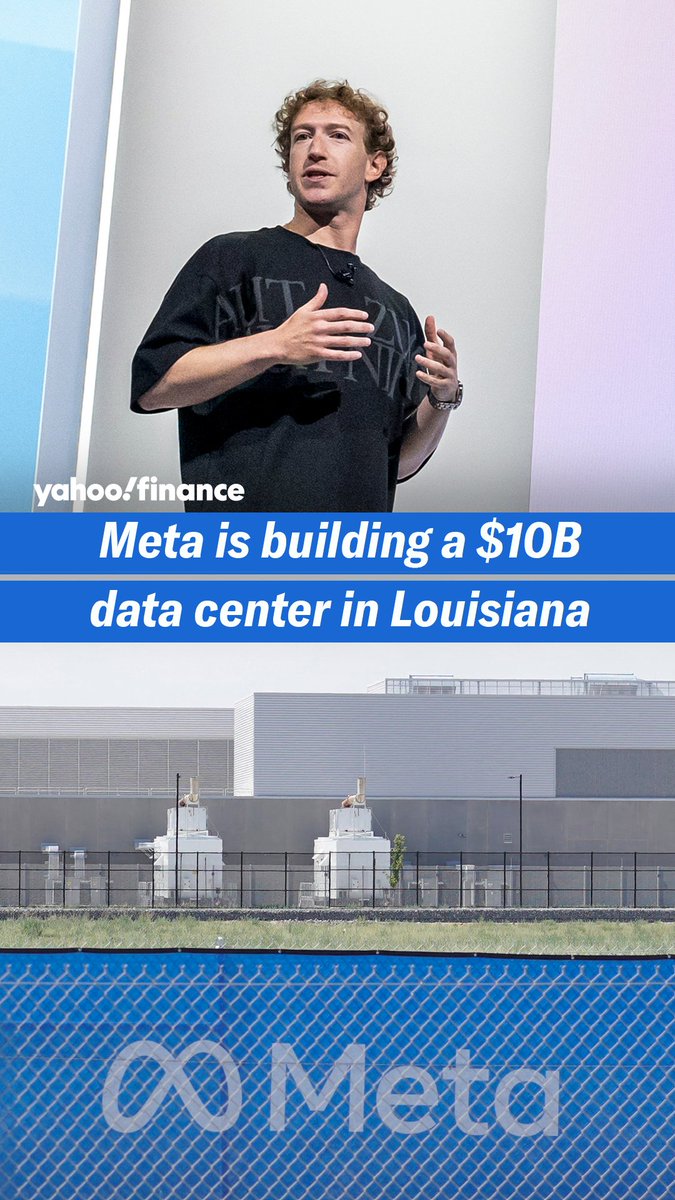

SITUATION EXPLAINED: OpenAI is leasing a 10-gigawatt data center. • Largest operational data centers today: ~1.2 gigawatts • OpenAI's planned campus: 10 gigawatts • Total cost: at least $500 billion if fully built out • All four hyperscalers combined are spending ~$700 billion this year • OpenAI has raised... show more

25,889 Aufrufe • vor 21 Tagen •via X (Twitter)

0 Kommentare

Keine Kommentare verfügbar

Kommentare vom Original-Post werden hier angezeigt